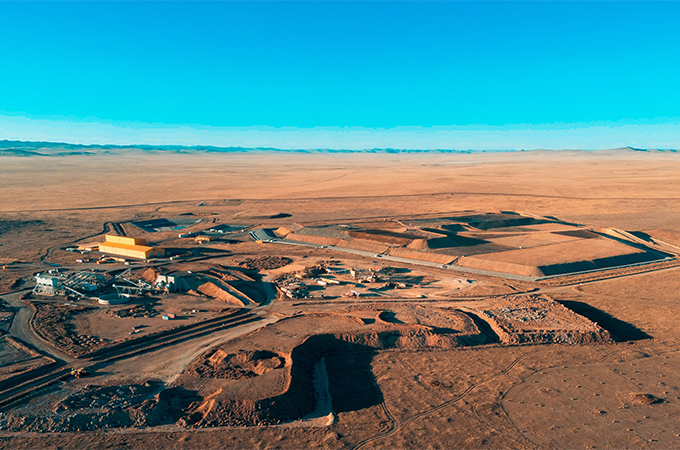

Image courtesy of Steppe Gold

Boroo Gold, Mongolia’s first hard-rock gold mine and the country’s first mining project financed by a foreign investor, has been recently bought by Steppe Gold, currently one of only a few gold producers in the country. Boroo was in production for 13 years before its former owner, Canadian company Centerra Gold, sold it, together with the Gatsuurt development property, to Singaporean-based OZD in 2018. While in production, Boroo poured 1.5 million oz of gold. Steppe has already produced over 100,000 oz from its Mongolian ATO project, and the acquisition would make Steppe the leading gold producer in the country.

This is only one among other promising news stories concerning the Mongolian copper-gold mining scene in the last two years, after more than a decade where not enough happened. Of course, the start of the Oyu Tolgoi (OT) underground development, which will propel the project to 500,000 t/y copper by 2028, is the most significant development in the last year. But besides this milestone, there are other important stories about Mongolia’s polymetallic porphyries: Xanadu Mines, an Australian-listed developer, received US$35 million from Chinese giant Zijin Mining Group to fund the Kharmagtai copper-gold project to pre-feasibility study. Steppe itself was the recipient of a first-of-its-kind loan of US$150 million from Mongolia’s largest bank, the Trade and Development Bank, to accelerate phase-2 underground expansion at its 2.4 million oz ATO gold mine. Next in line to start producing gold is Steppe’s Canadian peer, Erdene Resource Development (ERD), also freshly financed with US$40 million by the Mongolian Mining Corporation (MMC).

For a country with two of the largest copper mines in the world, copper-gold OT and copper-molybdenum Erdenet, Mongolia plays a minuscule role in global copper supply, while in gold it is only the 37th gold producer in the world, according to the World Gold Council. Even though Mongolia has an estimated copper reserve of over 1 billion t, according to the National Bureau of Asian Research (NBR), only two of the country’s mines are producing. It is unclear when Mongolia’s third largest copper mine, the Tsaagaan Suvraga Copper-Molybdenum mine of Mongolyn Alt Corporation (MAK), will come into production.

A big chunk of Mongolia’s copper is in the government’s hands with the Erdenet Mine, the exclusive copper producer before the OT and with a capacity to produce over 400,000 t/y of copper. The country’s gold, on the other hand, is mostly mined by artisanals. ‘Ninja’ miners and small-scale miners account for the largest part of the 19.4 t of gold that Mongolia produces yearly. Planet Gold Mongolia, a project led by the UN, estimates that between 40,000 to 60,000 people, a third of whom are women, are engaged in artisanal mining across 14 out of 21 provinces in Mongolia. This number represents about 12-20% of the labor force and is equal to the number of people employed in formal mining (60,000, according to the World Mining Congress).

The lack of exploration over the last decade explains why there are so few producers of copper and gold. According to Algirmaa Ikhbayar, CEO of Geosan, a local airborne geophysical company, between 2000 and 2012, US$300 million was circulated in the exploration sector alone. The current mines, few as they are, are the result of that previous cycle or stem from the exploration conducted by the Russians during the Soviet era.

The problem with having just one mega-project and very few explorers and developers is that it leaves Mongolia without global mid-tier miners, said Julien Lawrence, managing director of O2 Mining, a mining services company and operator of the Chuulut fluorspar mine. “The position I put to the government regularly is that, instead of relying on one big project, it should aim for 10 medium-size projects, with a pipeline of another 10 that are at the funded development stage. Out of 100 licenses issued, one can expect a single mine to develop, so the industry needs enough licenses to generate continuous supply and breed the opportunity for discovery and turning the discovery into development and eventually a mine.”

Colin Moorhead, the CEO of Xanadu Mines, has a similar message to the government: “What I would say to the government is that without juniors to advance projects, they’ll struggle to attract majors to invest billions.”

No juniors, no majors, Moorhead said in a panel at a 121 Event and exemplified how companies like Zijin invested in Mongolia on the back of Xanadu, just as Ivanhoe Mines grew through Rio Tinto’s intervention early on.

At an investment valued at US$15 billion that is finally moving towards full production, the OT might help to catalyze more exploration investment. The Central Asian Orogenic Belt that crosses Mongolia might be seeing another wave of exploration, so far discrete, as a handful of private companies are currently raising funds internally before going public. The Belt is believed to be the highest-grade group of Paleozoic porphyry deposits currently known in the world, according to an article published in Science Direct (Porter, 2015). The south of the country has become a hotspot for copper exploration, inspired no doubt by the immense discovery of the OT as well as MAK’s Tsaagaan Suvraga 240 million tons Cu-Mo. Gobi Venture, an early private explorer, came across copper, gold, lithium, fluorspar, molybdenum, and rare earths in the Gobi Desert at its Naran project, a copper-molybdenum porphyry deposit typical of the area. Two years ago, Xanadu also acquired a second project, Red Mountain, where it identified an attractive porphyry Cu-Au system, consolidating its position in the copper-gold porphyry Dornogovi district.

Just a few days ago, Xanadu entered a binding term sheet to add a third project to its portfolio, this time looking further west, with two licenses (Sant Tolgoi) in the Zavkhan province of Western Mongolia, a region known for copper-nickel (Cu-Ni systems). In that same area, junior private company Asian Battery Minerals identified Cu-Ni mineralization in the Gobi Altai province, a project that earned its place in the BHP Xplor program. This confirms a trend of copper explorers venturing into the west of the country, a region that has been active for gold.

Western Mongolia hosts the country’s main gold projects, including Steppe’s ATO, Boroo, and Gatsuurt projects, as well as Max Group’s Khan Altai project, the biggest in the Western region. Also in Western Mongolia, more precisely in the Bayankhongor Province, sits ERD’s Bayan Khundii gold deposit; 16 km away from Bayan Khundii, ERD secured a license for the Altan Nar exploration project in 2020.

While the south of the country benefits from a better-developed infrastructure, with available roads and power, the west will require more investment from the developers. Max Group, the group behind Khan Altai, is planning to build a coal-fired power plant in the region this year. This could be the largest such project in Western Mongolia, according to its executives. “The success of the Khan Altai project is pivotal for bringing modern infrastructure to this region, which, despite being connected to the Western power grid, faces capacity limitations. The company has ventured into developing both renewable energy and conventional power stations, although the latter faces financing challenges,” commented Davaa-Ochir Dashbaatar, managing director of the Mining and Heavy Industry Division at Max Group.

Generally, however, exploration costs are low in the country, says Dashbaatar, echoed by other executives. They refer to a low-cost labor force, about five to eight times lower compared to Australia or Canada, but also to the conditions on the ground, where there is little vegetation, few clouds, and therefore fewer interruptions, except for the harsh winters, the only time when exploration stops (usually for a month or two). Production costs are also competitive, with the OT looking to move into the C1 cost curve in the next five years. The cost challenge comes in the ramp-up from open pit to underground, since most deposits grow in size and grade at depth. At the OT, the grade will increase from 0.4% in the open-pit to 1.24% in the underground. Gold projects present the same characteristic; Steppe has been mining from to the oxide to date, but the bulk of the resource is in the fresh rock, so its Phase 2 development will consist of an underground operation that will allow it to ramp up to over 100,000 oz/y. Similarly, 80% of Khan Altai’s resource is in the sulfide, so its owners are also preparing for a Phase 2 development which will require a higher capex.

Almost all of the explorers and developers we talked to rely on debt, rather than equity. More than being a non-dilutive option, listed companies are also paying the costs of operating in a jurisdiction perceived as risky: “Mongolia is still a frontier market with associated investment risks. As a company primarily focused on Mongolia, our market cap is affected by the challenges that come with operating in this market. The talks between Mongolia’s government and Rio Tinto about the Oyu Tolgoi project have had positive and challenging phases, impacting the performance of Mongolian mining shares. However, over the past decade, anti-mining sentiment has notably decreased,” commented Bataa Tumur-Ochir, chairman and CEO of Steppe Gold.

Copper, and, often in association but not always, gold, remain Mongolia lowest-hanging fruit in the current climate. It was Rio Tinto’s biggest bet, having invested in Mongolia more than anywhere else outside of its home base in Australia. Unlike coal, copper demand is there to stay, while gold has rarely disappointed as an investment option. Mongolia has a copper-gold advantage thanks to its geology, proven to deliver fabulously when properly studied, but also this is the commodity space where the country has the most dynamic sector and a pipeline of projects that should turn into mines in the next years. Mongolian operators need to seize the momentum and deliver quickly before the tide turns – as seen in the past, commodity cycles can have a devastating effect on a country so profoundly tied to its minerals sector.

Image courtesy of Steppe Gold

Boroo Gold, Mongolia’s first hard-rock gold mine and the country’s first mining project financed by a foreign investor, has been recently bought by Steppe Gold, currently one of only a few gold producers in the country. Boroo was in production for 13 years before its former owner, Canadian company Centerra Gold, sold it, together with the Gatsuurt development property, to Singaporean-based OZD in 2018. While in production, Boroo poured 1.5 million oz of gold. Steppe has already produced over 100,000 oz from its Mongolian ATO project, and the acquisition would make Steppe the leading gold producer in the country.

This is only one among other promising news stories concerning the Mongolian copper-gold mining scene in the last two years, after more than a decade where not enough happened. Of course, the start of the Oyu Tolgoi (OT) underground development, which will propel the project to 500,000 t/y copper by 2028, is the most significant development in the last year. But besides this milestone, there are other important stories about Mongolia’s polymetallic porphyries: Xanadu Mines, an Australian-listed developer, received US$35 million from Chinese giant Zijin Mining Group to fund the Kharmagtai copper-gold project to pre-feasibility study. Steppe itself was the recipient of a first-of-its-kind loan of US$150 million from Mongolia’s largest bank, the Trade and Development Bank, to accelerate phase-2 underground expansion at its 2.4 million oz ATO gold mine. Next in line to start producing gold is Steppe’s Canadian peer, Erdene Resource Development (ERD), also freshly financed with US$40 million by the Mongolian Mining Corporation (MMC).

For a country with two of the largest copper mines in the world, copper-gold OT and copper-molybdenum Erdenet, Mongolia plays a minuscule role in global copper supply, while in gold it is only the 37th gold producer in the world, according to the World Gold Council. Even though Mongolia has an estimated copper reserve of over 1 billion t, according to the National Bureau of Asian Research (NBR), only two of the country’s mines are producing. It is unclear when Mongolia’s third largest copper mine, the Tsaagaan Suvraga Copper-Molybdenum mine of Mongolyn Alt Corporation (MAK), will come into production.

A big chunk of Mongolia’s copper is in the government’s hands with the Erdenet Mine, the exclusive copper producer before the OT and with a capacity to produce over 400,000 t/y of copper. The country’s gold, on the other hand, is mostly mined by artisanals. ‘Ninja’ miners and small-scale miners account for the largest part of the 19.4 t of gold that Mongolia produces yearly. Planet Gold Mongolia, a project led by the UN, estimates that between 40,000 to 60,000 people, a third of whom are women, are engaged in artisanal mining across 14 out of 21 provinces in Mongolia. This number represents about 12-20% of the labor force and is equal to the number of people employed in formal mining (60,000, according to the World Mining Congress).

The lack of exploration over the last decade explains why there are so few producers of copper and gold. According to Algirmaa Ikhbayar, CEO of Geosan, a local airborne geophysical company, between 2000 and 2012, US$300 million was circulated in the exploration sector alone. The current mines, few as they are, are the result of that previous cycle or stem from the exploration conducted by the Russians during the Soviet era.

The problem with having just one mega-project and very few explorers and developers is that it leaves Mongolia without global mid-tier miners, said Julien Lawrence, managing director of O2 Mining, a mining services company and operator of the Chuulut fluorspar mine. “The position I put to the government regularly is that, instead of relying on one big project, it should aim for 10 medium-size projects, with a pipeline of another 10 that are at the funded development stage. Out of 100 licenses issued, one can expect a single mine to develop, so the industry needs enough licenses to generate continuous supply and breed the opportunity for discovery and turning the discovery into development and eventually a mine.”

Colin Moorhead, the CEO of Xanadu Mines, has a similar message to the government: “What I would say to the government is that without juniors to advance projects, they’ll struggle to attract majors to invest billions.”

No juniors, no majors, Moorhead said in a panel at a 121 Event and exemplified how companies like Zijin invested in Mongolia on the back of Xanadu, just as Ivanhoe Mines grew through Rio Tinto’s intervention early on.

At an investment valued at US$15 billion that is finally moving towards full production, the OT might help to catalyze more exploration investment. The Central Asian Orogenic Belt that crosses Mongolia might be seeing another wave of exploration, so far discrete, as a handful of private companies are currently raising funds internally before going public. The Belt is believed to be the highest-grade group of Paleozoic porphyry deposits currently known in the world, according to an article published in Science Direct (Porter, 2015). The south of the country has become a hotspot for copper exploration, inspired no doubt by the immense discovery of the OT as well as MAK’s Tsaagaan Suvraga 240 million tons Cu-Mo. Gobi Venture, an early private explorer, came across copper, gold, lithium, fluorspar, molybdenum, and rare earths in the Gobi Desert at its Naran project, a copper-molybdenum porphyry deposit typical of the area. Two years ago, Xanadu also acquired a second project, Red Mountain, where it identified an attractive porphyry Cu-Au system, consolidating its position in the copper-gold porphyry Dornogovi district.

Just a few days ago, Xanadu entered a binding term sheet to add a third project to its portfolio, this time looking further west, with two licenses (Sant Tolgoi) in the Zavkhan province of Western Mongolia, a region known for copper-nickel (Cu-Ni systems). In that same area, junior private company Asian Battery Minerals identified Cu-Ni mineralization in the Gobi Altai province, a project that earned its place in the BHP Xplor program. This confirms a trend of copper explorers venturing into the west of the country, a region that has been active for gold.

Western Mongolia hosts the country’s main gold projects, including Steppe’s ATO, Boroo, and Gatsuurt projects, as well as Max Group’s Khan Altai project, the biggest in the Western region. Also in Western Mongolia, more precisely in the Bayankhongor Province, sits ERD’s Bayan Khundii gold deposit; 16 km away from Bayan Khundii, ERD secured a license for the Altan Nar exploration project in 2020.

While the south of the country benefits from a better-developed infrastructure, with available roads and power, the west will require more investment from the developers. Max Group, the group behind Khan Altai, is planning to build a coal-fired power plant in the region this year. This could be the largest such project in Western Mongolia, according to its executives. “The success of the Khan Altai project is pivotal for bringing modern infrastructure to this region, which, despite being connected to the Western power grid, faces capacity limitations. The company has ventured into developing both renewable energy and conventional power stations, although the latter faces financing challenges,” commented Davaa-Ochir Dashbaatar, managing director of the Mining and Heavy Industry Division at Max Group.

Generally, however, exploration costs are low in the country, says Dashbaatar, echoed by other executives. They refer to a low-cost labor force, about five to eight times lower compared to Australia or Canada, but also to the conditions on the ground, where there is little vegetation, few clouds, and therefore fewer interruptions, except for the harsh winters, the only time when exploration stops (usually for a month or two). Production costs are also competitive, with the OT looking to move into the C1 cost curve in the next five years. The cost challenge comes in the ramp-up from open pit to underground, since most deposits grow in size and grade at depth. At the OT, the grade will increase from 0.4% in the open-pit to 1.24% in the underground. Gold projects present the same characteristic; Steppe has been mining from to the oxide to date, but the bulk of the resource is in the fresh rock, so its Phase 2 development will consist of an underground operation that will allow it to ramp up to over 100,000 oz/y. Similarly, 80% of Khan Altai’s resource is in the sulfide, so its owners are also preparing for a Phase 2 development which will require a higher capex.

Almost all of the explorers and developers we talked to rely on debt, rather than equity. More than being a non-dilutive option, listed companies are also paying the costs of operating in a jurisdiction perceived as risky: “Mongolia is still a frontier market with associated investment risks. As a company primarily focused on Mongolia, our market cap is affected by the challenges that come with operating in this market. The talks between Mongolia’s government and Rio Tinto about the Oyu Tolgoi project have had positive and challenging phases, impacting the performance of Mongolian mining shares. However, over the past decade, anti-mining sentiment has notably decreased,” commented Bataa Tumur-Ochir, chairman and CEO of Steppe Gold.

Copper, and, often in association but not always, gold, remain Mongolia lowest-hanging fruit in the current climate. It was Rio Tinto’s biggest bet, having invested in Mongolia more than anywhere else outside of its home base in Australia. Unlike coal, copper demand is there to stay, while gold has rarely disappointed as an investment option. Mongolia has a copper-gold advantage thanks to its geology, proven to deliver fabulously when properly studied, but also this is the commodity space where the country has the most dynamic sector and a pipeline of projects that should turn into mines in the next years. Mongolian operators need to seize the momentum and deliver quickly before the tide turns – as seen in the past, commodity cycles can have a devastating effect on a country so profoundly tied to its minerals sector.